Research in behavioral economics over the past few decades has shown that people’s decisions often deviate from those of “homo-economicus,” the selfish rational agent who is the hero of most economic theory textbooks. These deviations (also known as “decision biases”) often lead to suboptimal outcomes in the individual and the societal levels and have become the target of various policy interventions.

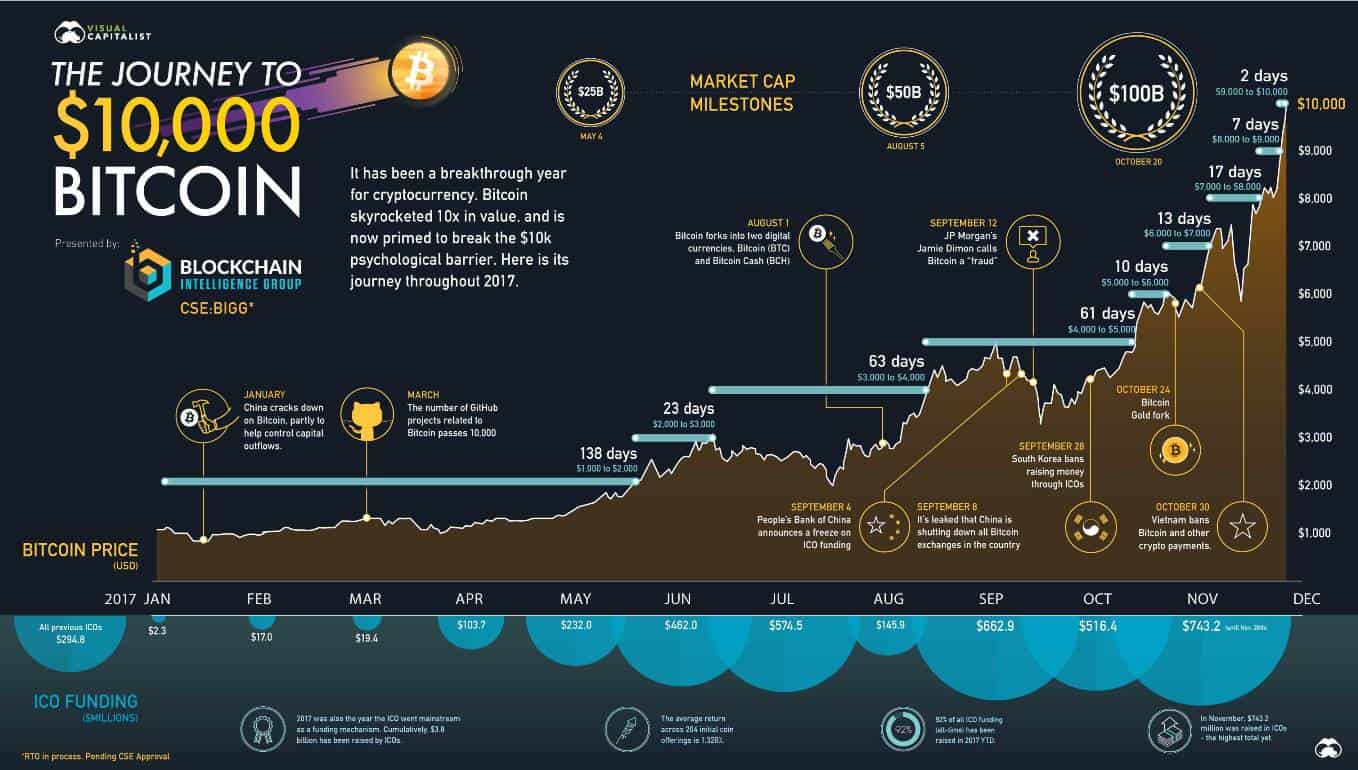

For instance, in 2017, Bitcoin reached $10,000. While the figure $10,000, by itself, doesn’t deliver much beyond the fundamental price information, this number had significant psychological implications. Because humans generally think in round numbers, hitting the $10,000 threshold has become an important event that made it to the front page of the evening news.

Behavioral economists have characterized many other systematic decision biases that unlikely reflect arbitrary mistakes. But what is causing them?

Contemporary humans face decision problems that are quite different from those that our ancestors had encountered. Deciding whether to go hunting or foraging for grains is different from choosing between 30 types of barbecue sauce on the supermarket shelf; forecasting tomorrow’s rainfall based on today’s weather is not the same as predicting tomorrow’s Bitcoin prices based on today’s market. As our brains have evolved in environments that do not resemble modern markets, we might rely on assumptions that are no longer optimal when making economic decisions.

In contrast to financial decision-making, humans seem to make reliable judgments and decisions in the perceptual domain. Although sensory illusions are pervasive in carefully controlled experiments under unnatural settings, people are remarkably good at making sense of perceptual information as they navigate the chaotic world outside the laboratory. Past documentation of a visual illusion in the field, a photo of a blue dress that seemed white to the majority of the population, was regarded with so much astonishment, that it became a worldwide internet sensation overnight. As our brains have evolved in an environment governed by the same regularities that operate today (i.e., mechanical, optical, and acoustic physical laws), we still benefit from relying on the same computations that our ancestors’ brains had used when making decisions that translate sensory information into perceptual judgments and motor actions.

The year 2017 was a good one for Bitcoin. While the world was Bitcoin crazed, one Nobel Prize winner economist felt that Bitcoin offers a psychological experiment more than it provides investment opportunities.

“I’m interested in Bitcoin as a sort of bubble. It doesn’t mean that it will disappear, that it’ll burst forever. It may be with us for a while,” Noble Prize winner Robert Shiller, professor of economics at Yale University and co-founder of the Case-Shiller Index, told CNBC’s “Trading Nation.”

“To me, it’s interesting as another example of faddish human behavior. It’s glamorous,” he added.

The Bitcoin rush took Shiller back in history when the tulip mania was in swing. It was the 17th century, and the prices of tulip bulbs peaked to new heights, but later crashed in 1637. This was the first recorded event that demonstrated a bubble due to buyers’ frenzy that threw the prices higher than the real value of the product.

Many decision processes in the financial domain have parallels in the perceptual domain. Our sensitivity to light intensity and auditory loudness follows logarithmic laws that resemble the manner in which we encode monetary rewards. We perceive the luminance and size of objects about their surroundings, in way that resembles framing effects in economic decision-making. Even the compromise and the attraction effects, well-documented phenomena in consumer decision-making, were recently documented in the perceptual domain. These findings suggest that decision biases might arise because our brains apply computational techniques that successfully solve perceptual problems, also when making economic decisions.

A recent study, co-authored by Cary Frydman (USC) and yours truly, investigated the common mechanism across the economic and perceptual domains in the context of specific decision bias, the extrapolative formation beliefs, also known as the belief in the “hot hand”. People often rely on past observations when forecasting the future, even when they contain no credible information. This tendency is thought to underlie market-level phenomena such as over-reaction to news and creation of a price bubble, like in the case of Bitcoin.

Intriguingly, extrapolative belief formation is also often found in laboratory experiments of perceptual decision-making: people respond faster and more accurately to sensory stimuli that continue an apparent pattern, even when explicitly told that the sequence is completely random. In the study, Cary and I used a within-subject design, where each participant took part in decision-making tasks from both the economic and perceptual domains.

Our goal was to investigate whether people use a common computational mechanism of belief formation when making both types of decisions. This was a test of a 16 years old idea of the above mentioned Robert Shiller, who wrote in his seminal book “Irrational Exuberance”:

“The same human pattern-recognition faculty that we used when we learned to ride a bike or to drive a car, giving us an intuitive sense of what to expect next, shapes our expectations for the market.”

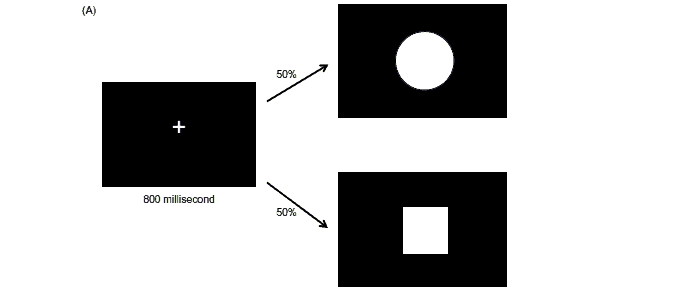

In the perceptual decision-making task (figure below), we asked participants to make a series of perceptual decisions. Every round of the task started with the appearance of a fixation cross in the middle of the screen, which after 800 milliseconds was replaced by either a circle or a square. The chance of seeing either shape was always 50% and did not depend on history. Participants had to classify the shape by pressing the “left” button when it was a circle, and “right” when it was a square. They received money whenever they classified the shape accurately, and the faster they did so.

We found that when a shape continued a “streak” of similar shapes (for example, a circle appeared after three other circles), participants were more likely to classify it correctly, and were also faster when doing so. This suggests that the participants were implicitly forming expectations about the identity of the next stimulus based on past observations, despite being explicitly told that the sequence was random.

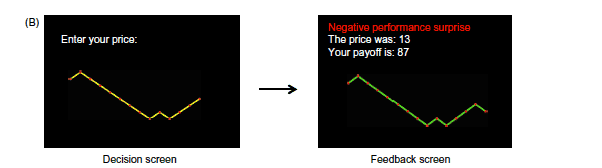

In the economic task (figure below), participants saw a series of events that represented “performance surprises” of a publicly traded firm. These events could be either “positive” or “negative.” Each round, we asked participants to decide how much they were willing to pay for a stock that would be worth $100 if the next performance surprise were “positive,” but $0 if it were negative. In this case, it was optimal for them to pay the dollar amount that equals the probability that (according to one’s belief) the next performance surprise would be positive. The participants did not know that the actual sequence of performance surprises was completely random: the actual probability of seeing either a positive or negative surprise was 50% and did not depend on the history at all.

In this task, Cary and I found that after a sequence of several “positive” performance surprises, participants were willing to pay more for the stock, and the longer the streak was, the more they were willing to pay. After a sequence of “negative surprises, they were willing to pay less, and again, the longer the streak was, the less they were willing to pay. This suggests that just participants were forming expectations about the future based on past observations, and were doing so in a similar fashion to the perceptual task.

Most intriguingly, we found a reliable correlation between the degree of extrapolative beliefs across the perceptual and economic tasks. In other words, people who responded faster and more accurately to a “circle” that preceded a series of other circles (compared to a “square” that preceded a series of circles), despite being explicitly told that the shapes appeared at random, were also more likely to bid more money for a stock of a firm that had a recent streak of positive performance surprises

Our findings may partly explain the pattern of prices in the “psychological experiment” of Bitcoin trading in 2017. As the price went up, more and more people were eager to buy Bitcoin, thinking that the rise will continue. The same happens these days, in the bear market of 2018-2019, as the volume of sellers increases as Bitcoin price goes down – leading to a negative momentum which is unrelated to the currency’s fundamental value.

These results illuminate the origins of extrapolative belief formation in economic decision-making. Humans might be relying on low-level automatic processes that play a role in perceptual decision-making when forming their economic judgments. If this is the case, the formation of extrapolative beliefs might be a cognitive process which is difficult to suppress.

{kind=link}

{kind=link}

{kind=link}